Executive Summary

The management of false positives across sanctions, politically exposed persons, and adverse media screening is one of the most significant sources of operational inefficiency in compliance functions across regulated industries. This case study examines how spektrQ deployed a custom AI screening agent for a large financial institution to restructure the false positive review process – reducing per-case review time, enabling risk-adjusted automation of high-confidence determinations, and eliminating redundant screening of shared beneficial owners across the institution's client portfolio.

Problem Statement

Screening individuals and entities against sanctions lists, PEP databases, and adverse media sources is a mandatory component of anti-money laundering and know-your-customer compliance programmes. The challenge is not the screening itself – it is the volume of false positive alerts that screening generates and the manual review burden this places on compliance teams.

A screening alert is generated whenever a potential match is identified between a screened individual and a record in a sanctions or PEP database. Many of these matches are false positives: a shared name, a partial date of birth match, or a geographic association that is incidental rather than material. For common names in particular, a single screening run can generate hundreds of individual alerts, each of which must be reviewed against the underlying source data to determine whether it represents a genuine match or an irrelevant coincidence.

In the manual review model, each alert is assessed individually. An analyst must read the source record, evaluate the match criteria across multiple dimensions – name, date of birth, nationality, associated entities – and document a determination. For an institution screening thousands of individuals and entities across onboarding and ongoing monitoring cycles, this produces a substantial and recurring demand on analyst capacity, the majority of which is directed at alerts that will ultimately be dismissed as false positives.

A further and compounding dimension of the problem is entity duplication. Where the same ultimate beneficial owner appears across multiple client relationships – a common occurrence in institutional portfolios – the conventional approach requires that the screening process be run independently for each client relationship in which that individual appears. The same UBO may be screened, reviewed, and cleared multiple times across different onboarding processes, generating redundant work with no incremental compliance value.

Solution

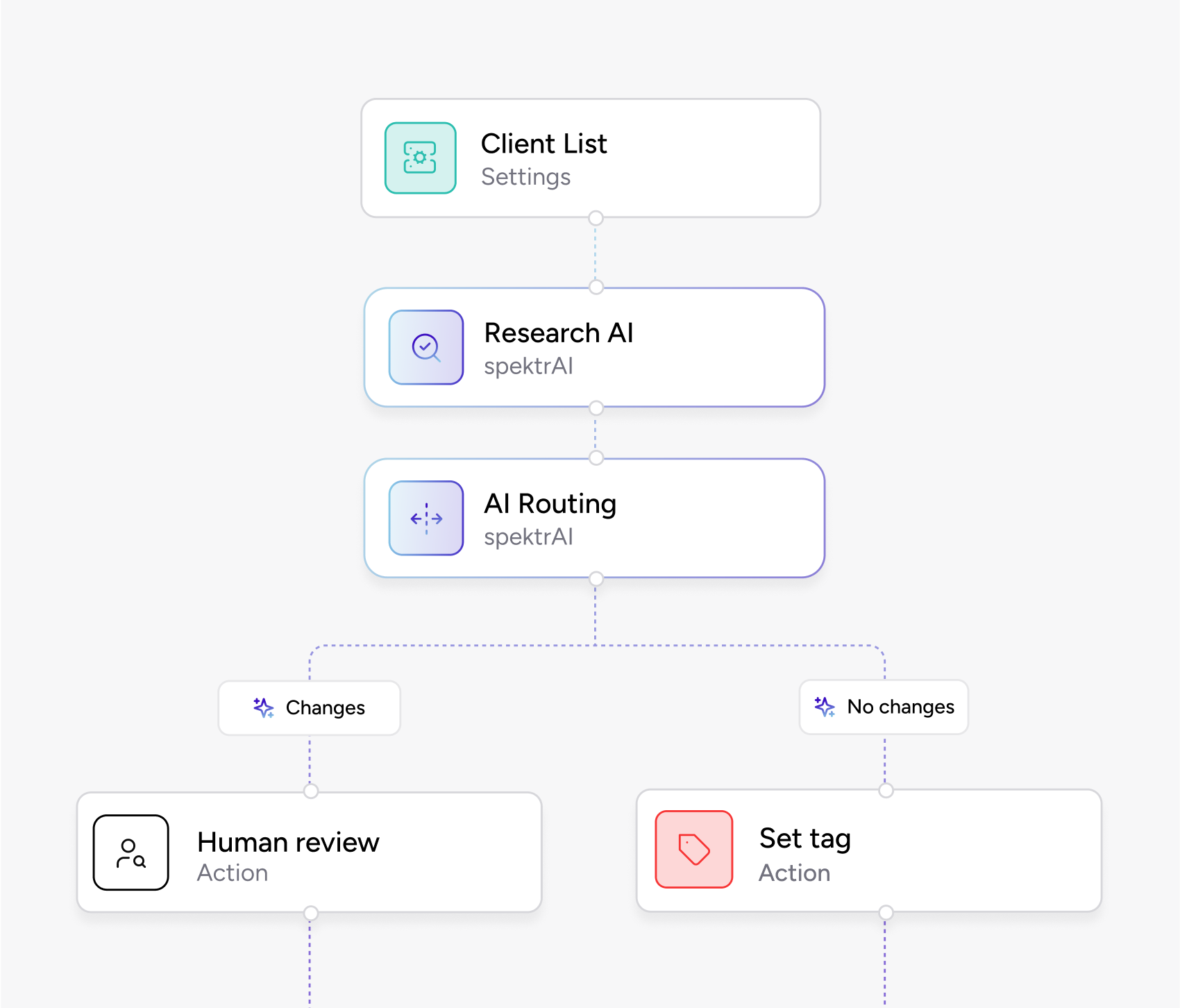

spektrQ deployed a custom AI screening agent designed to address the false positive problem at two levels: alert grouping and entity deduplication.

At the alert grouping level, the agent processes the full set of screening alerts generated for a given individual or entity and organises them into thematic clusters based on the nature of the underlying match. Rather than presenting an analyst with hundreds of individual alerts, the agent presents a structured summary of alert clusters. Each cluster includes a description of the match category, a consolidated review of the relevant source data from the screening provider, a summary of the key match and non-match criteria, and an aggregate confidence assessment classified as low, medium, or high.

The analyst reviews the cluster summary rather than the individual alerts. A determination made at the cluster level resolves all alerts within that cluster simultaneously, substantially compressing the review process. For high-confidence determinations – where the agent's assessment meets the institution's defined confidence threshold – the institution can configure automatic resolution, with the full alert record retained for audit purposes. Institutions with lower risk tolerance maintain full analyst review but benefit from the structured presentation and the elimination of redundant individual alert assessments.

At the entity deduplication level, the agent maintains a cross-portfolio register of screened and cleared beneficial owners, confirmed by a unique identifier such as a national identity number or social security number. Where a UBO who has been recently screened and cleared appears in a new client relationship, the existing screening record is applied rather than initiating a new screening run. The UBO continues to be monitored on an ongoing basis, but the one-time review burden of initial screening is not repeated without cause.

Technical Approach

The screening agent was integrated with the institution's existing screening service providers via API, enabling it to receive alert data and apply the grouping and summarisation logic before alerts are presented to the analyst review queue. The grouping taxonomy and confidence thresholds were configured in collaboration with the institution's compliance team during an initial pilot phase, during which all agent determinations were reviewed by analysts to validate performance before automated resolution was enabled for high-confidence cases.

The deduplication layer was built as a modular component of the same workflow, maintaining a continuously updated register of screened entities that is queried at the point of each new screening run. Identity confirmation is handled through a defined verification protocol using unique identifiers, ensuring that deduplication is applied only where identity can be established with certainty.

Outcomes

The deployment produced a material reduction in the volume of individual alerts requiring direct analyst review. By resolving alerts at the cluster level rather than the individual level, per-case review time was reduced significantly. Analysts reported a marked improvement in the clarity and usability of the review process, with structured summaries and consolidated source references eliminating the preparatory work previously required before a determination could be made.

The deduplication component eliminated a significant proportion of redundant screening runs across the portfolio, with the greatest impact observed in client segments with high levels of shared beneficial ownership. Compliance team capacity was effectively expanded without an increase in headcount, with time redirected toward complex cases, model validation, and regulatory engagement.

Conclusion

False positive management in sanctions and PEP screening is a problem that only grows with portfolio size and compounds with regulatory complexity. The manual review model that most institutions operate today is not viable at the volumes that modern compliance obligations demand. AI-driven alert grouping, risk-adjusted automation, and entity deduplication offer a technically defensible and regulatorily robust path to resolving this challenge – one that augments analyst judgment rather than replacing it, and that produces outcomes that are fully auditable and configurable to each institution's specific risk appetite.